AMN Healthcare — Looking Beyond the Aya Index

Insight into the Latest Travel Nurse and Allied Healthcare Staffing Trends from Alternative Data Sources

Before we dive into another post on my favorite levered healthcare shitco that most people couldn’t care less about, I have a couple of housekeeping items.

For starters, I’d like to apologize for the month-long gap between posts — at first my excuse was going to be that the recent warm weather distracted me…but then disaster struck. After finishing this post on Tuesday, Substack decided that it was going to delete it and not save any prior drafts. I initially contemplated hurling myself out of the car on I-95 rather than rewriting it all again, but here I am for a second time, just with a tad more hostility. My dedication to shitco research is unwavering. You’re welcome. (For those of you who are concerned for my personal wellbeing, I’ve realized the right approach is to write these posts on Microsoft Word first to prevent another deletion disaster).

Also, given what’s going on in the world today, I feel compelled to say this — every word written in my posts is me shooting from the hip in my own voice. I will never use ChatGPT to speak my shitco truths and I aim to be as authentic as possible. If you see my excessive usage of “—” and think that means I used ChatGPT, you’re wrong. I just forget how to properly use semicolons and take the easy way out.

Anyway, without further ado…

One thing I realized from the feedback on my first post on macro and micro industry trends in contract labor spending is that most people did not appreciate how unprecedented it is to have the level of detail that we do for individual hospital contract labor spending. As previously discussed, contract labor typically accounts for 2-3% of a hospital’s spending on salaries, wages and benefits (“SWB”) — or roughly 1-2% of revenue — in a normalized labor environment. Most companies do not bother to break out costs that are only 1-2% of revenue and that’s been true historically for contract labor as well. That would be like companies disclosing how much they spend on toilet paper and office supplies.

This all changed in 2021 due to the pandemic when contract labor spending increased over 200% and blew up the PNLs of many hospitals — Wall Street research analysts began asking about it on every earnings call, management teams began proactively calling it out as a headwind (and later as a tailwind) to earnings, and shareholders, bondholders and rating agencies of public and non-profit health systems began requesting more details on the underlying contract labor spending trends. That said, the disclosure is still somewhat selective, loosely quantitative, and requires knowing where to dig. To create a time series and industry level mosaic from pre-Covid to today wasn’t like downloading data from FactSet, Bloomberg or a table in a 10K — it was a pain in the ass, but one worth doing since it 1) is an analysis that very few people (if any) were doing, and 2) confirmed my view that the healthcare staffing industry is set to inflect positively for the first time in 3 years.

However, while that contract labor spending analysis and industry commentary provides us with confidence in a high-level thesis, it’s equally helpful to monitor the various public data sources that provide more real-time insight into demand and bill rate trends within the healthcare staffing industry. The goal of this post is to lay out how current trends are shaping up and what it means for my favorite shitco, AMN Healthcare Services (NYSE: AMN). So let’s get started.

What are Current Expectations?

Thanks to numerous acquisitions in adjacent healthcare staffing verticals over the last 10 years, as well as a significant decline in its travel nurse staffing business, AMN Healthcare is more diversified today than ever. In 2022 at the height of the pandemic, AMN derived approximately 2/3rds of total revenue from travel nurse staffing, and ~80% combined from travel nurse and allied healthcare staffing. In Q1 2025, ~37% was from travel nursing and ~60% was from travel nurse and allied staffing combined. This compares to ~50% for travel nursing and ~72% for nurse and allied staffing combined pre-Covid.

Why does this matter? Because despite <40% of revenue (and ~25% of gross profit) coming from travel nurse staffing, it is still the primary driver of the stock. Given my work (and management’s commentary) suggests that travel nurse staffing is currently ~20% below pre-Covid levels on a volume basis, any improvement on the that side of the business would provide material upside to the stock.

As it stands today, AMN’s stock is down over 80% from 2022 and ~65% vs pre-Covid because of revenue that has declined ~20% every quarter since Q1 2023, and EBITDA that is down ~75% from the pandemic peak. Investors likely need to see a sustainable inflection in the travel nurse staffing business before they’re willing to step in, and although current estimates for H2 2025 bake in some improvement, nobody believes it.

In the below chart you can see that the rate of y/y declines in AMN’s travel nurse business is projected to improve by over 10% in Q2 2025, a noteworthy inflection vs the prior 9 quarters. While this guidance might seem aggressive, data I track suggests we are possibly tracking slightly ahead of those seemingly high Q2 expectations.

Further, consensus estimates for Q3 2025 bake in another large step function acceleration which most investors are skeptical of. My goal with this post is to use recent data trends from multiple publicly available sources to highlight why AMN is right on track.

The Aya Index

Aya Healthcare is the largest healthcare staffing firm in the US with a market share somewhere in the high-teens as of 2024. Within the travel nursing and allied healthcare verticals they have ~25% and ~20% market share, respectively. The company is privately held, has grown incredibly quickly (>100% revenue CAGR from 2018-2022), and has been disrupting the healthcare staffing industry through a combination of lower bill-pay spreads (i.e., lower margins) and industry-leading technology solutions.

Given Aya’s scale within the industry and their executive presence on the expert networks, their publicly available “Aya Index” is the most widely followed demand barometer in the healthcare staffing industry. You can access it here.

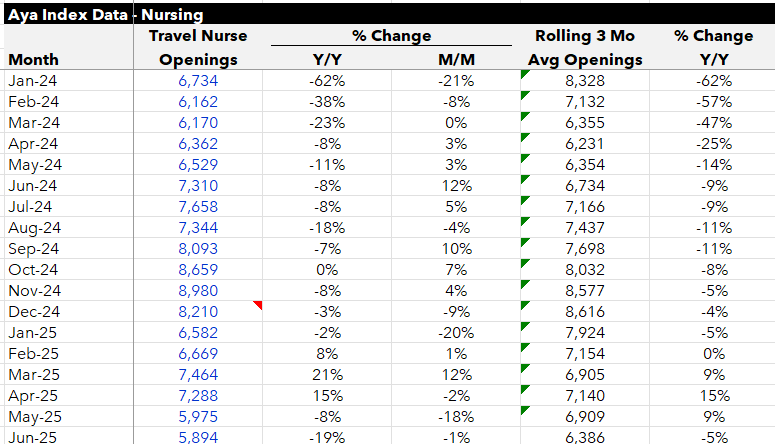

The index provides weekly updates on travel nurse and allied healthcare job openings based on Aya’s internal data including “direct contracts, managed service contracts and support of third-party staffing programs”. The data looks like this:

As it relates to AMN Healthcare, ~60% of LTM revenue is derived from travel nurse and allied healthcare staffing so investors treat these weekly Aya updates as gospel —in fact, you’ll very likely see AMN’s stock react positively or negatively when the Aya Index data has a noteworthy positive or negative inflection. However, there are obvious limitations to this data as a read-thru for AMN, including:

Aya has been a share gainer since 2018 so job opening increases may reflect that and not be relevant for AMN.

Every staffing firm has exclusive contracts with large health systems and those specific system trends will impact open orders for that specific staffing firm. For example, AMN derives 23% of its nurse and allied staffing revenue from one single customer, Kaiser Permanente. Therefore, Kaiser’s hiring trends will have an outsized impact on AMN’s demand compared to whatever is shown in the Aya Index. Similarly, any customer losses specific to Aya would reduce their job openings but have no read-thru to AMN.

The Aya Index is job openings only, not filled jobs. “Fill Rate” is an important metric that fluctuates based on several factors including available nurse supply, pay rates, attractiveness of open jobs (e.g., certain specialties are more desirable), whether a job opening is exclusive via MSP or open for bidding, etc. Having lots of job openings at low pay rates will lead to a lower fill rate as nurses won’t be interested in taking those roles and therefore more orders does not necessarily translate to more revenue. An open job filled directly by the staffing firm via an MSP arrangement (e.g., AMN places a nurse at a hospital) has a much larger revenue and gross profit contribution than an open job filled via a vendor management take rate arrangement (e.g., AMN takes a 3-5% cut of gross spend for a job filled by a different staffing agency through their vendor management system).

Aya does not provide insight into bill rates.

Aya does not provide insight into international travel nurse trends which represents ~15% of AMN’s travel nurse business and is ~1,500bps higher gross margin than their US nurse staffing business.

In terms of correlations, the Aya Index data is loosely predictive at best and has a large absolute error, so while it’s an ok proxy for industry demand trends, it should not be as impactful as it is in terms of driving AMN’s stock price in the short term.

All that being said, here’s what the Aya Index has been telling us this year.

After 33 straight months of declines, travel nurse job openings increased in February 2025 (+8% y/y) for the first time since April 2022.

In March 2025 travel nurse job openings accelerated to +21% y/y but then decelerated to +15% in April 2025.

Travel nurse job openings then began declining again in May 2025 (-8% y/y) and have now posted the worst y/y decline since early 2024 so far in June 2025 (-19%).

Allied healthcare job openings posted strong y/y growth of +25% in January-April 2025, an acceleration from 2024, but then massively decelerated in May 2025 (+6% y/y), and started declining in June (-2% y/y).

While it’s unclear what the exact reasoning is for the recent negative inflection in Aya’s job openings, the timing does correlate with Trump’s tariff induced economic uncertainty as well as the proposed Medicaid cuts in his new spending bill.

Below is a time series of the rolling 3 month travel nurse job openings since 2020 showing the positive inflection in 2025 prior to Trump’s “Liberation Day”.

Despite this recent deceleration in Aya’s travel nurse job openings, I’m not convinced it’s affecting AMN to the same degree. Since Aya, AMN and all of the large staffing firms are in the business of filling jobs, they have websites where they list each individual job opening. See here for Aya and here for AMN. The trend in job openings on their websites shows a very different story for Aya and AMN — Aya’s travel nurse job openings on their website mirror the trend shown in their disclosed Aya Index while AMN’s travel nurse job openings show a more stable reality.

The websites for the other large healthcare staffing firms (Faststaff/Ingenovis, Medical Solutions/Host, Nomad, Cross Country, TNNA, and Prolink) show a similarly stable trend suggesting that the Aya deceleration is more likely company specific.

Also recall what AMN management said on the Q1 2025 earnings call which they reported on May 8th: